Should You Lock in a Mortgage Rate Now or Wait for Rates to Drop?

Buyers across Irvine and Orange County are asking the same question right now:

Is it better to lock in a mortgage rate today or wait for potential decreases?

With mortgage rates stabilizing after several volatile years, the decision in December 2025 is less about timing the market and more about managing risk, affordability, and local market conditions.

Quick Summary

- Mortgage rates are currently in the low-to-mid 6 percent range.

- Most forecasts expect only modest changes, not major drops.

- Locking now is often safer for buyers closing soon.

- Waiting may make sense for buyers with flexible timelines.

- A rate lock with a float-down option can offer protection with flexibility.

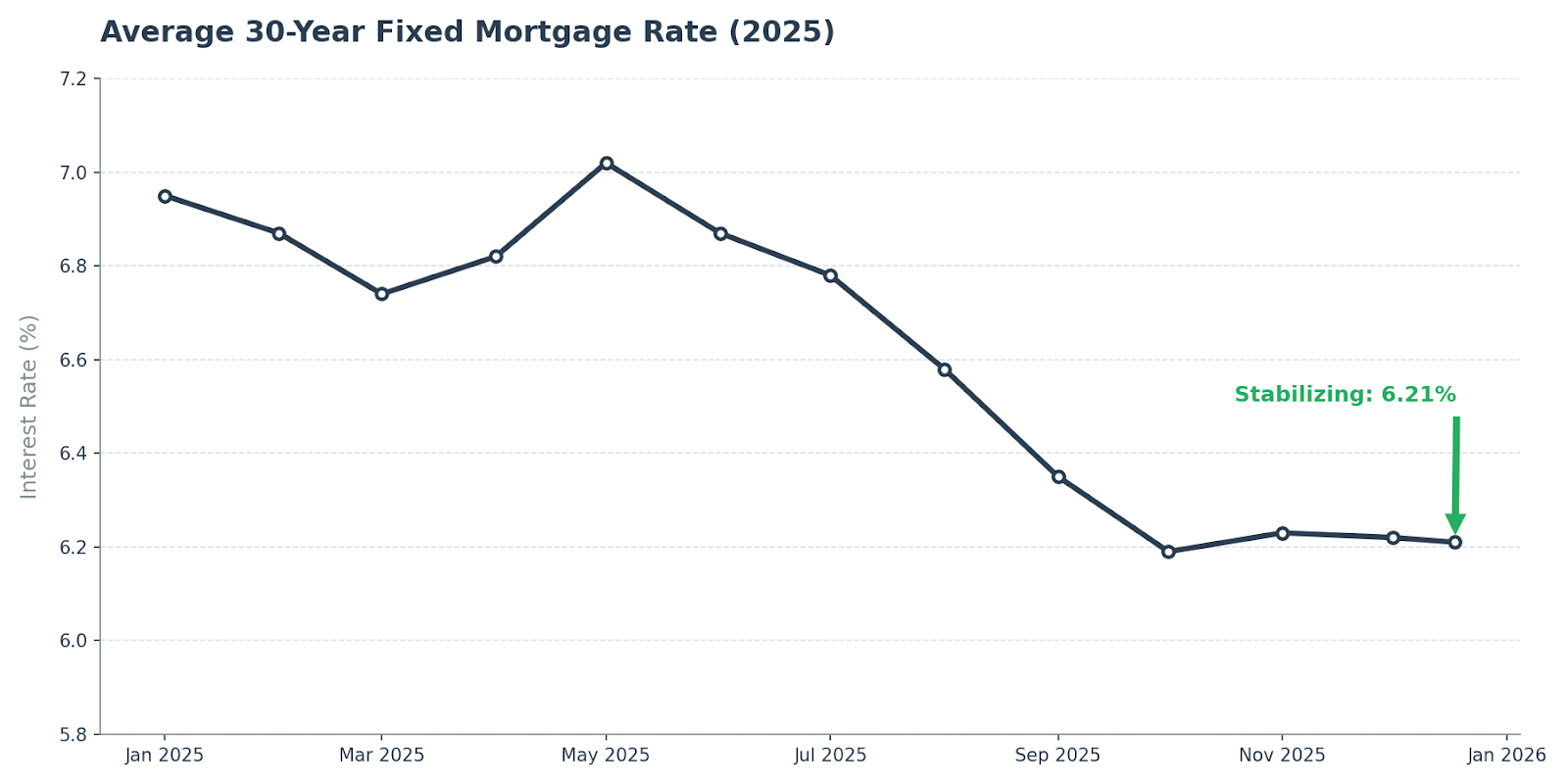

Current Mortgage Rates in December 2025

As of mid-December 2025, average 30-year fixed mortgage rates are hovering around 6.2 to 6.3 percent. Rates have moved off earlier highs but have not resumed a steady downward trend.

This period of relative stability changes the conversation. Instead of chasing rate drops, buyers need to decide whether today’s payment works within their long-term budget.

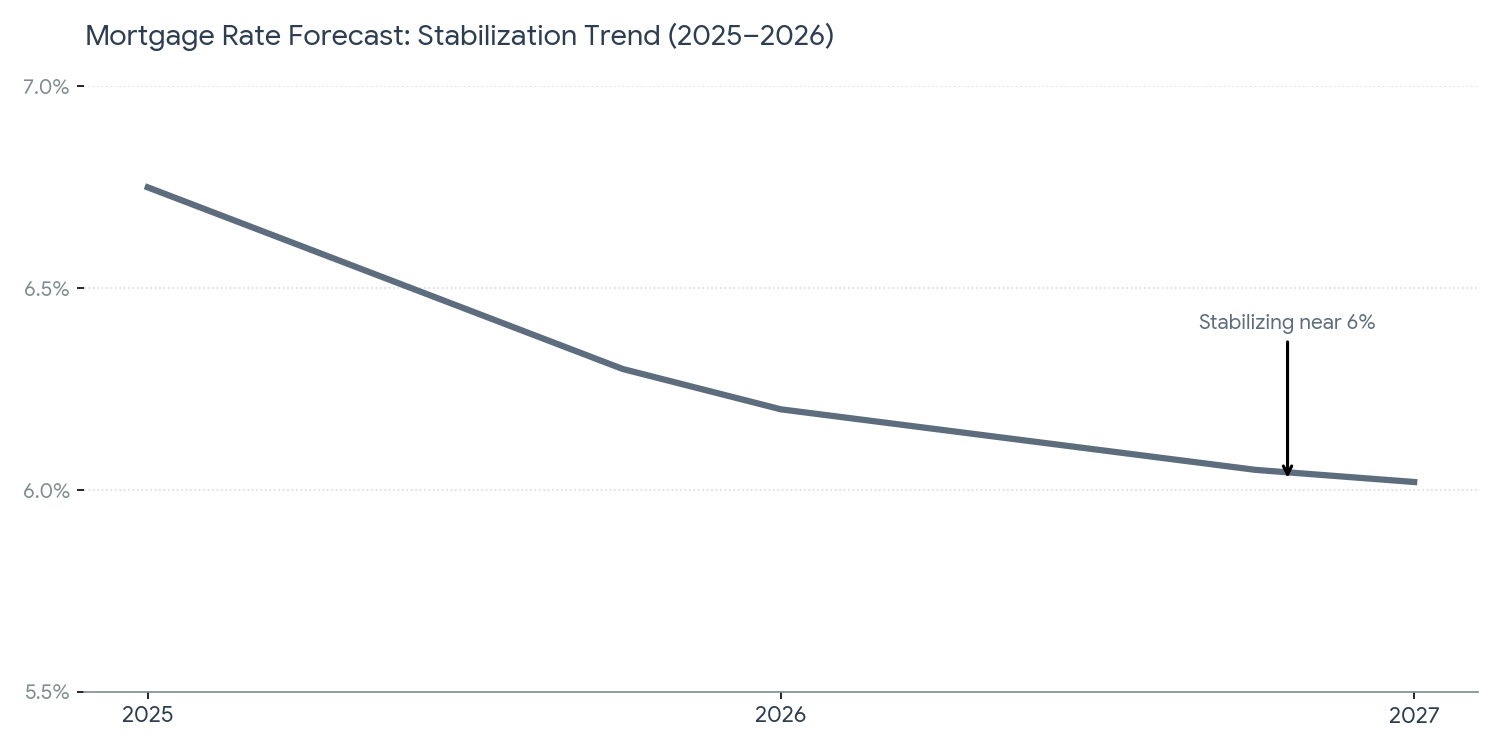

What Mortgage Rate Forecasts Are Saying

Most major housing and lending organizations expect limited movement in mortgage rates going forward.

- Rates are generally projected to remain between about 5.9 percent and 6.5 percent.

- Gradual easing is possible, rather than sharp declines.

- There is no widespread expectation of a return to historically low mortgage rates.

This means buyers waiting for dramatic drops are likely to be disappointed.

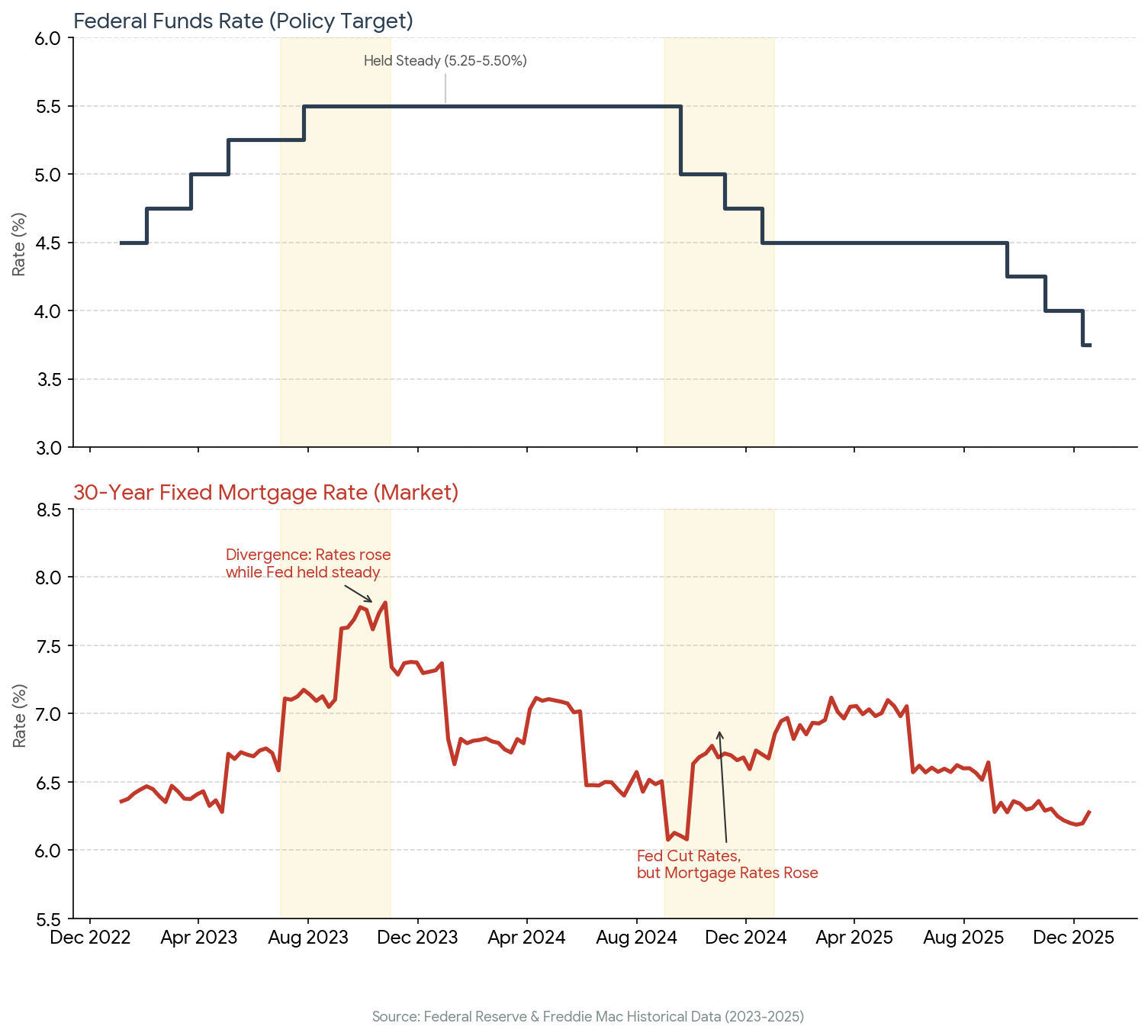

Why Federal Reserve Cuts Do Not Guarantee Lower Mortgage Rates

A common misconception is that mortgage rates fall automatically when the Federal Reserve cuts interest rates.

In reality, mortgage rates are influenced more by inflation expectations, the 10-year Treasury yield, and the long-term economic outlook.

Even after multiple Fed cuts in 2025, mortgage rates remained elevated because long-term bond yields stayed high. This is why buyers should not wait for a single Fed announcement to make borrowing suddenly cheaper.

Why Locking a Mortgage Rate Now Often Makes Sense

For many buyers, locking a mortgage rate now is the safer and more predictable choice.

- The upside of waiting is usually small.

- The downside of rates rising can be meaningful.

- Locking protects your monthly payment and loan approval.

- Certainty reduces stress during escrow.

For buyers near the top of their budget, even a small rate increase can affect qualification or comfort.

Local Market Conditions in Irvine and Orange County

National data only tells part of the story. Local conditions matter.

In many areas of Irvine and Orange County, housing inventory remains limited. When buyers wait, prices can rise, competition can increase, and seller flexibility can decline.

In these markets, a slight rate improvement can be offset by a higher purchase price.

When Locking Now Is Usually the Better Choice

Locking your rate now often makes sense if:

- You plan to close within 30 to 60 days.

- Today’s payment fits comfortably in your budget.

- A rate increase would strain your debt-to-income ratio.

- You prefer certainty over speculation.

- You are buying in a competitive local market.

When Waiting or Floating Can Be Reasonable

Waiting may be reasonable if:

- Your timeline is six to twelve months out.

- Even a small rate improvement would materially change affordability.

- You are comfortable with the risk of rates staying flat or rising.

- Your local market conditions allow patience.

This approach requires realistic expectations and flexibility.

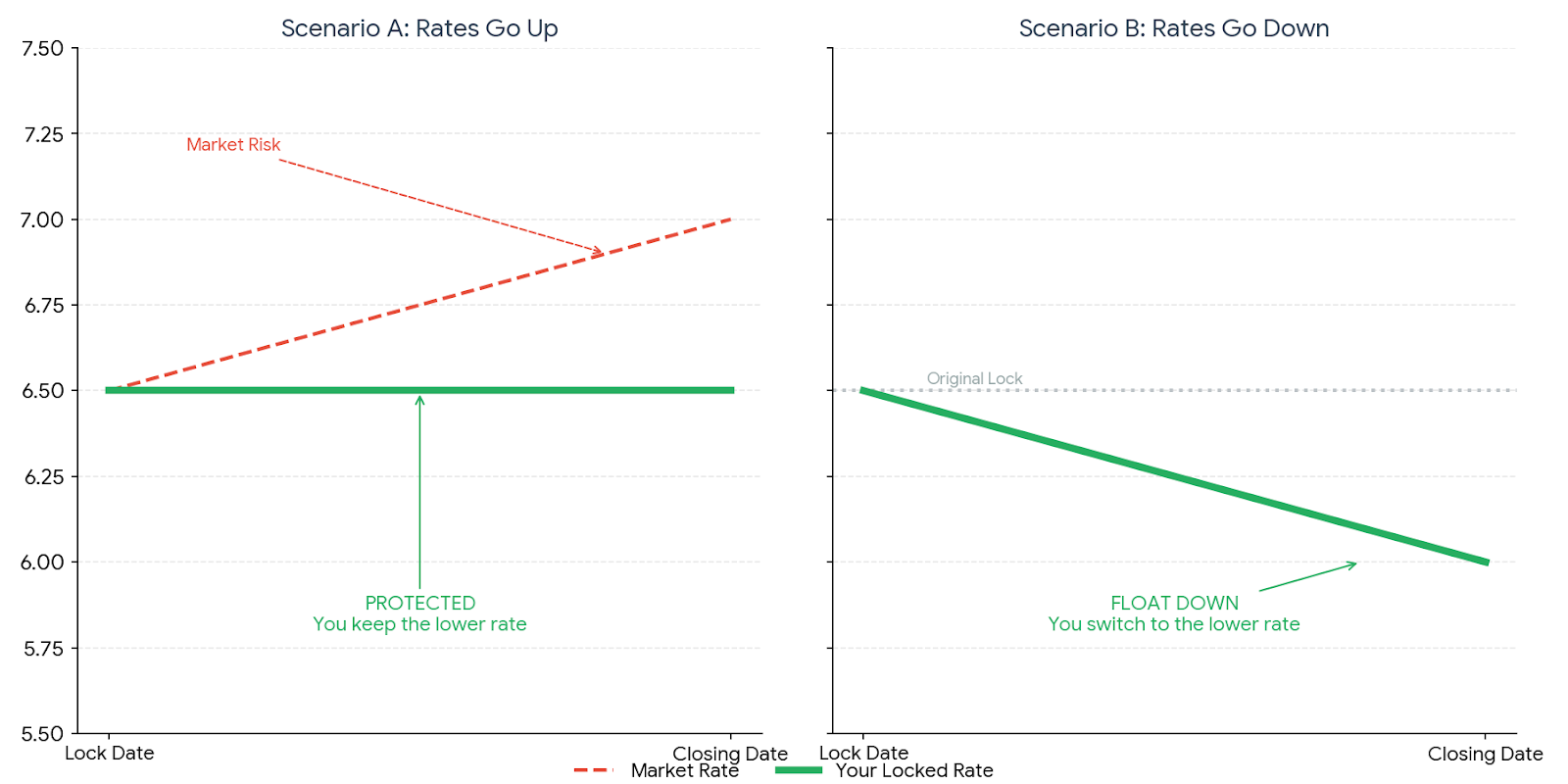

The Middle Ground: Lock With a Float-Down Option

A rate lock with a float-down option allows buyers to lock today’s rate to protect against increases while keeping limited upside if rates fall before closing.

Availability and cost vary by lender, so this should be discussed early in the loan process.

Mortgage Rate Lock FAQs

Is it better to lock in a mortgage rate now or wait?

For most buyers in December 2025, locking now is safer due to stable rates and limited forecasted declines.

Will mortgage rates go down in 2026?

Most forecasts expect rates to remain near 6 percent, with only modest declines possible.

Do mortgage rates follow Federal Reserve rate cuts?

No. Mortgage rates are driven more by inflation expectations and long-term Treasury yields.

Should I lock my rate if I am closing soon?

Yes. Locking helps protect your payment and loan approval from short-term volatility.

What is a mortgage rate float-down option?

It allows you to lock now and move to a lower rate if rates drop before closing, subject to lender rules.

Is waiting for lower rates risky?

Yes. Rates may rise, and in competitive markets like Irvine and Orange County, prices may increase while you wait.

Can I refinance later if rates fall?

Yes. Refinancing is typically an option if rates drop meaningfully, though costs apply.

Final Takeaway

Mortgage rates in late 2025 suggest stability rather than major opportunity.

For most buyers in Irvine and Orange County, locking in a mortgage rate now offers protection and peace of mind. If rates improve later, refinancing is an option. Stretching your budget or missing the right home is far harder to undo.

Debbie Sagorin

Sagorin & Associates

Coldwell Banker Realty