By Debbie Sagorin, REALTOR® - Coldwell Banker Realty, Newport Beach

California DRE #01411020 | ABR®, CNE, e-PRO®, Smart Home Certified | RealTrends Verified (2026) | 22+ yrs Orange County, 350+ closed (250+ Irvine), Top 1% Irvine | 12-time Five Star Award | 285+ verified reviews | 840 Newport Center Drive #100, Newport Beach, CA 92660 | +1-949-537-2079 | [email protected]

Published: September 22, 2025 | Updated: June 16, 2026

Update Note (June 2026):

This article was originally published in September 2025 when mortgage rates dropped from roughly 7% to 6.3%. The rate, payment, and quote figures below reflect that period. For current Orange County and Irvine market data, see my June 2026 Woodbridge market update and the latest weekly market posts. The structural affordability framework in this piece - rates, prices, wages - remains how I help buyers evaluate timing in any market.

Quick Answer

Housing affordability comes down to three forces: mortgage rates, home prices, and wages. When all three move in the buyer's favor at once - rates down, price growth slowing, paychecks rising - even a modest shift can lower a typical monthly payment by hundreds of dollars. In fall 2025, the average 30-year fixed dropped from roughly 7% to 6.3%, cutting an $800,000 mortgage payment by about $380 per month from rates alone. For Irvine and Orange County buyers, the takeaway is the same in any cycle: re-run your numbers whenever rates move 50+ basis points, because the same home can become reachable without the price changing at all.

From My Files (Fall 2025):

In May 2025 I worked with a Stonegate-area family who had been pre-approved at the spring rate near 7%. They walked through three Eastwood Village and Stonegate homes and ran the math at the kitchen counter each time. The monthly payment on the home they actually loved came in about $400 above what they were comfortable carrying. They paused. When rates dipped into the low-6s that September, I called them, re-ran the same home at the new rate, and the payment landed inside their comfort zone. They re-engaged within a week, made an offer on a Stonegate property, and closed before Halloween. Nothing about the house, the price, or their income had changed - only the rate. That is the practical lesson behind every "affordability" headline: small moves in rates change what is buyable for real families, in real Irvine villages, on real timelines.

In Irvine and across the country, it's been tough for many homebuyers over the past couple of years to make the numbers work. Home prices rose sharply. Mortgage rates did too. For some, that meant pressing pause on their home search because it just didn't feel possible. Maybe you were one of them.

The good news? If you've been waiting for a better time to get back into the market, affordability is finally starting to show signs of improvement this fall.

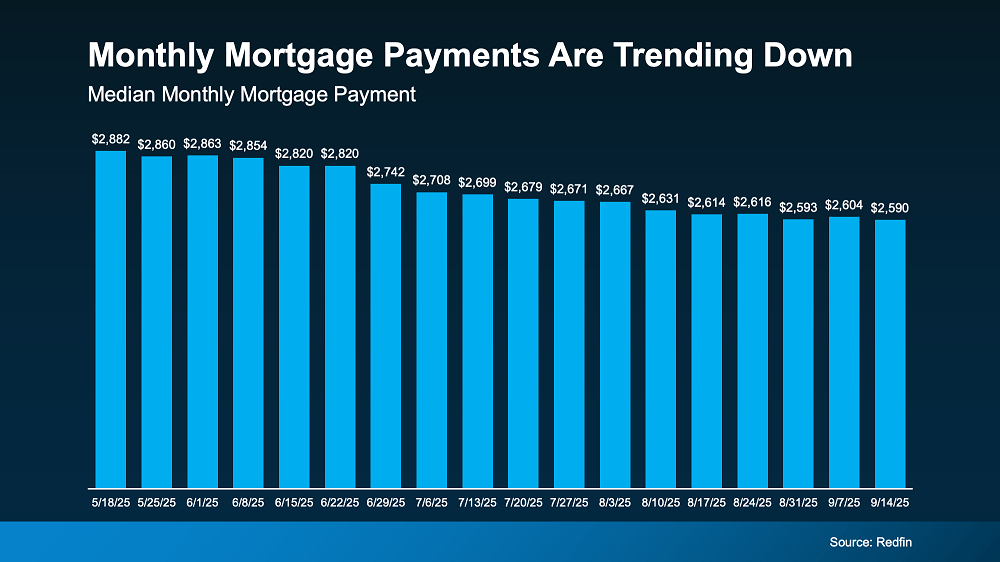

The latest data from Redfin shows the typical monthly mortgage payment has been coming down, and is now about $290 lower than it was just a few months ago (see graph below):

And here's why this is happening. The cost of buying a home really comes down to three things:

Mortgage rates

Home prices

Your wages

Right now, all three are finally moving in a better direction for you. While that doesn't mean it's suddenly easy to buy at today's rates and prices, it does mean it's not as challenging.

1. Mortgage Rates

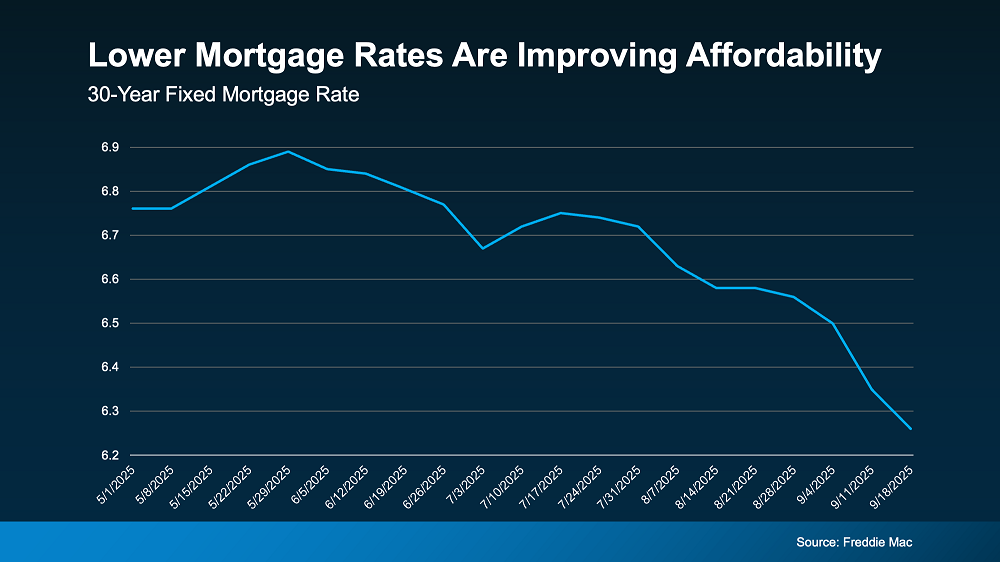

Mortgage rates have come down compared to earlier this year. In May, they were roughly 7%. And now, they're closer to 6.3% (see graph below):

That may not sound like a big deal, but it does matter. Even small changes in rates can make a difference in your future monthly payment. Compared to when rates were 7%, if you take out an average $800K mortgage now at 6.3%, it'll cost about $380 less a month based on just rates alone.

And for some people, that's been enough to make buying a home possible again. As Joel Kan, VP and Deputy Chief Economist at the Mortgage Bankers Association (MBA), explained on September 10th:

"The downward rate movement spurred the strongest week of borrower demand since 2022 . . . Purchase applications increased to the highest level since July and continued to run more than 20 percent ahead of last year's pace."

2. Home Prices

After several years of prices rising very rapidly, price growth has finally slowed. As Odeta Kushi, Deputy Chief Economist at First American, puts it:

"National home price growth remains positive, but muted, low single digits, and we expect this trend to continue in the second half of the year."

For buyers, that's actually a big relief. That moderation makes it easier to plan your budget. And in some Orange County markets, prices have even dipped slightly. If you're in one of the markets, you may be able to find something that's more affordable than you'd expect.

3. Wages

According to the Bureau of Labor Statistics (BLS), wages are up near 4% annually. Lawrence Yun, Chief Economist at NAR, explains why that number is so important right now:

"Wage growth is now comfortably outpacing home price growth, and buyers have more choices."

In other words, the typical paycheck is rising faster than home prices right now, which helps make buying a little more affordable. Now, it's not a big difference, but in a market like this, every bit counts.

What This Means for Irvine Buyers (and Others, of Course)

Lower rates, slower price growth, and stronger wages might be enough to make the numbers finally work for you this fall.

While affordability is still tight, it's a little easier on your wallet to buy now than it was just a few months ago. Remember, data from Redfin shows the typical monthly mortgage payment is already around $290 lower than it was earlier this year country-wide, so in Orange County that gap is much larger in dollar terms.

Bottom Line

If you've been thinking about buying in Irvine or anywhere in Orange County, it may be worth taking another look this fall.

Let's run the numbers together. We can review your budget, see what's changed, and figure out if this is the season to turn window-shopping into key-turning.

How the Three Affordability Drivers Are Tracked

Three federal and industry datasets sit behind every affordability headline. Knowing where the numbers come from helps you separate signal from noise:

- Mortgage rates are tracked weekly by Freddie Mac's Primary Mortgage Market Survey (PMMS), the longest-running benchmark for the 30-year fixed rate in the United States. PMMS surveys lenders each week and reports the average rate for a conforming loan with 20% down.

- Home prices are tracked nationally by the FHFA House Price Index, which measures repeat-sale prices on properties with conforming mortgages. It is the cleanest like-for-like price measure because it follows the same homes through multiple sales rather than comparing different houses.

- Wages are tracked monthly by the Bureau of Labor Statistics Current Employment Statistics, which reports average hourly earnings across private-sector industries. When BLS shows wage growth running faster than FHFA shows price growth, affordability is improving for the typical worker - even if rates have not moved.

When you read an affordability headline, check which of these three the article is actually measuring. Many "affordability is improving" stories rest on only one of the three moving.

More Questions About Housing Affordability in Irvine

Q1. How do mortgage rates affect the monthly payment more than the home price itself?

On a 30-year loan, the interest cost dominates the early years of the amortization schedule. On an $800,000 mortgage, moving from 7% to 6.3% reduces principal-and-interest by roughly $380 per month, which over 30 years is more than $136,000 in lifetime interest. Even a 0.5% rate move on a typical Irvine loan can shift the monthly payment by $200 to $300, which is often the difference between qualifying and not qualifying. That is why I tell buyers to re-run their numbers any time the 30-year fixed moves 50 basis points or more.

Q2. What is the 30-year fixed mortgage rate and where does the published number come from?

The "30-year fixed" you see in headlines is the average rate lenders are offering nationally on a conventional, conforming, 30-year fixed-rate mortgage. The most-quoted benchmark is Freddie Mac's Primary Mortgage Market Survey (PMMS), published every Thursday. Your actual rate will differ based on credit score, loan-to-value, loan amount, property type, and the lender you choose. In Irvine, where most loans are above the conforming limit, jumbo rates can run a quarter-point higher or lower than PMMS depending on the lender's appetite for those loans that week.

Q3. How does wage growth versus home price growth affect what I can afford?

If wages are growing faster than home prices, the typical household is gaining purchasing power even before rates move. The Bureau of Labor Statistics tracks average hourly earnings; the FHFA tracks home prices. When BLS year-over-year wage growth exceeds FHFA year-over-year price growth, affordability is structurally improving. In fall 2025 wages were up roughly 4% while home price growth had cooled to the low single digits, so the wage-to-price gap was finally working in buyers' favor for the first time since 2020.

Q4. Should I wait for rates to drop further before buying in Irvine?

I tell every client the same thing: marry the house, date the rate. If you wait for a rate floor that may or may not arrive, you are also waiting in a market where Irvine prices have historically recovered any short-term softness within 12 to 18 months. If rates drop further after you close, you refinance. If prices rise while you wait, you cannot un-do that. The right question is not "are rates at the bottom?" - the right question is "does this monthly payment fit my budget today, and can I see myself in this home for at least five years?"

Q5. What is a reasonable affordability rule of thumb for Orange County buyers?

The traditional 28/36 rule says housing should not exceed 28% of gross monthly income and total debt should not exceed 36%. In Orange County, where median home prices are well above the national figure, many buyers stretch closer to 35% on housing alone. That can work if your income is stable, your reserves are 6+ months, and you are not carrying other consumer debt - but it is the ceiling, not the goal. I run two scenarios with every buyer: the payment they qualify for and the payment they will actually enjoy living with. Those are rarely the same number.

Disclaimer: This article is for general educational purposes and reflects market conditions as published. It is not lending, tax, or legal advice. Mortgage rates, qualification standards, and pricing change daily and vary by lender, credit profile, and property. Always confirm current rates with a licensed loan officer and consult a tax or legal professional for advice specific to your situation. Real estate professionals do not set or guarantee mortgage rates.