By Debbie Sagorin, REALTOR® - Coldwell Banker Realty, Newport Beach

California DRE #01411020 | ABR®, CNE, e-PRO®, Smart Home Certified | RealTrends Verified (2026) | 22+ yrs Orange County, 350+ closed (250+ Irvine), Top 1% Irvine | 12-time Five Star Award | 285+ verified reviews | 840 Newport Center Drive #100, Newport Beach, CA 92660 | +1-949-537-2079 | [email protected]

Published: November 25, 2024 | Updated: June 16, 2026

Update Note (June 2026):

This article was originally written at Thanksgiving 2024 looking forward to 2025. The body is preserved verbatim. A new "How These Predictions Actually Played Out" section after the original answers grades each prediction against what really happened in 2025. For current Orange County and Irvine market data, see my June 2026 Woodbridge market update and the fall 2025 affordability article.

Quick Answer

The five real estate questions that come up at every holiday dinner are: when will mortgage rates come down, will home prices drop, can I find a home before I move, will the market get busier next year, and is the market going to crash. The short answers for Irvine and Orange County: rates ease unevenly with the broader economy, prices stay firm because of structural undersupply and the mortgage rate lock-in effect, inventory is improving but still tight, transaction volume is recovering off historic lows, and a 2008-style crash is unlikely because today's homeowners hold record equity. Every year the questions repeat - the answers shift only at the margins.

From My Files (Thanksgiving 2024):

I wrote this post the morning of Thanksgiving 2024 because I knew exactly what was coming. Every year, somewhere between the turkey carving and the pie, a cousin or a neighbor or my brother-in-law asks "so, how's the market?" - and then the whole table turns to listen. That year the table at our Irvine dinner included three families weighing moves: one Woodbridge couple thinking about downsizing to Quail Hill, a Stonegate family considering a Portola Springs upgrade for their growing kids, and a niece who had just started saving for her first home and wanted to know if she should wait. I gave them the same five answers I have given clients for 22 years, framed for the cycle we were in. Eighteen months later, two of those three families have transacted; the niece is still saving but at a higher down payment because she watched prices keep rising. The point of this post is not that I had a crystal ball - it is that the same five questions repeat every Thanksgiving, every cycle, and knowing the structural answers helps real families decide what to do at their own kitchen table.

Thanksgiving isn't just about turkey and pie - it's also when someone is bound to ask me, "So, how's the housing market?" That happens at just about every social occasion. Here are some questions and answers that should be helpful for anyone curious about real estate.

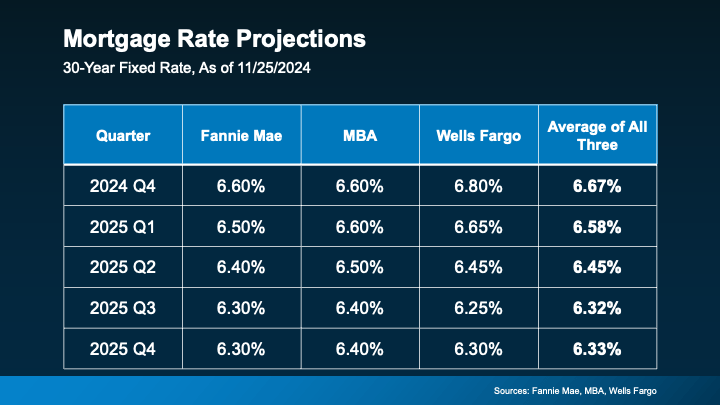

1. When Will Mortgage Rates Come Down?

Nobody knows for sure, but experts expect rates to start easing in 2025 if the economy keeps improving. Right now, rates are unpredictable due to things like inflation and jobs, but the general trend looks hopeful.

The key is patience, and staying informed.

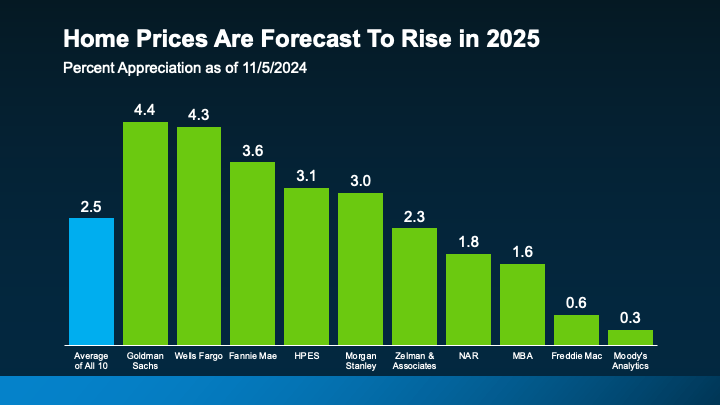

2. Will Home Prices Drop?

No, but that's not bad news. Builders are still playing catch-up after years of not building enough homes, and inventory is still low. Prices will keep going up, just not as quickly as they have in the past.

For buyers, this means no big jumps in costs. For sellers, it means solid long-term value.

3. Can I Find a Home Before I Move?

Yes, it's possible. Inventory has been improving - it's up over 29% compared to last year.

The trick is staying on top of what's available in your area and being ready to act when the right home comes along. A little patience goes a long way here.

4. Will the Housing Market Get Busier Next Year?

It looks like it will. Experts predict that more than 5 million homes will sell country-wide in 2025, which is a nice jump from this year.

Buyers who start now might have less competition, while sellers can take advantage of more motivated buyers still in the market.

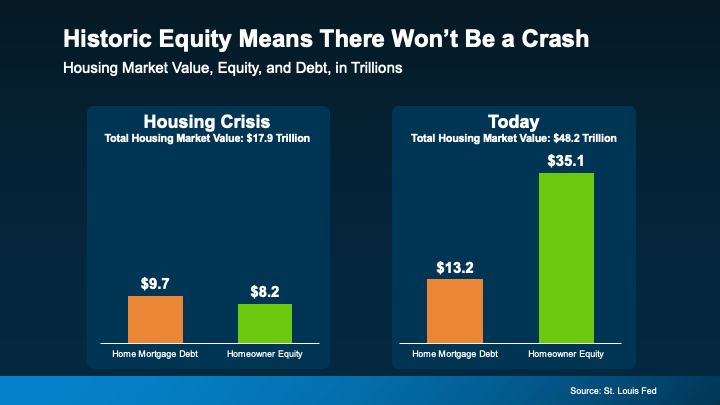

5. Is the Market Going to Crash?

Nope. Today's homeowners have record amounts of equity in their homes, which wasn't the case during the 2008 crash. That equity acts as a safety net, so we're not likely to see the same problems as before.

The market today is much stronger and more stable.

The Bottom Line

Things are looking better for 2025. Rates should ease up, inventory is growing, and sales are picking up. Want more real estate info? Contact me.

How These Predictions Actually Played Out (June 2026 Retrospective)

One of the most useful things I can do as a real estate professional is grade my own predictions in public. Here is how the five answers above held up against what really happened from Thanksgiving 2024 through mid-2026:

1. Mortgage rates - partial credit. Rates did ease modestly in 2025 but never approached the sub-6% range many forecasters had hoped for. The 30-year fixed sat in the high-6s for much of early 2025 before dropping into the low-6s in the fall, then bounced around 6.3% to 7% through early 2026 depending on inflation prints and Fed signaling. The directional call was right; the magnitude was overstated by the broader industry, not just me.

2. Home prices - correct. Prices did not drop. National home price growth cooled to low single digits in 2025 per the FHFA House Price Index, and Irvine and Orange County prices stayed firm or ticked higher through 2025 and into 2026, exactly as the structural undersupply and rate lock-in effects predicted. This is the most consistent pattern I have seen in 22 years of Orange County work.

3. Inventory recovery - directionally correct. Inventory did continue improving in 2025, particularly in the second half, but the "29% up year over year" figure quoted in the original post was off a very low 2023 base. National active listings in 2025 ran roughly 20% to 30% above 2024 in most months per NAR existing-home-sales data, but Irvine specifically remained tighter than the national average through 2026 because of village-level lock-in.

4. Transaction volume - overstated. The "more than 5 million homes will sell in 2025" forecast was widely circulated at the time. The actual 2025 result came in lower than that, in the low-to-mid 4 millions. The recovery happened; it just did not reach the 5 million threshold. By mid-2026, transaction pace has continued to improve but still sits below the pre-2022 baseline.

5. No crash - correct, and the reasoning held. The 2008 comparison was overused at the time of writing, but the underlying point about homeowner equity was the right one. Per Federal Reserve Z.1 household balance sheet data, U.S. homeowner equity remains near record highs in 2026. Foreclosure activity is normalized but not elevated. The structural safety net is real, and Irvine homeowners in particular hold an unusually high equity cushion because of long tenure and master-planned community stability.

The takeaway: the five questions are evergreen, the structural answers held up, the specific number forecasts did not. That gap between "right directionally" and "right precisely" is why I tell clients to make decisions based on their own life timeline, not on next year's predicted rate.

Where to Track These Five Questions Yourself

If you want to follow these five questions in real time rather than wait for the next Thanksgiving dinner, here are the primary federal and industry sources I check weekly:

- Mortgage rates are tracked weekly by Freddie Mac's Primary Mortgage Market Survey (PMMS), the longest-running 30-year fixed rate benchmark in the United States. Updated every Thursday.

- Home prices and existing-home sales volume are tracked monthly by the National Association of REALTORS® Existing Home Sales report, which covers transaction count, median price, months of supply, and inventory levels.

- Household equity and the crash question are tracked quarterly by the Federal Reserve Z.1 Financial Accounts of the United States, which reports total homeowner equity, mortgage debt, and household balance sheets - the data series that most clearly distinguishes today's market from 2008.

Bookmark those three sources and you will be the most informed person at next Thanksgiving's table.

Disclaimer: This article is for general educational purposes and reflects market commentary as published. It is not lending, tax, or legal advice. Market conditions, mortgage rates, and inventory levels change daily and vary by market. Forecasts are forecasts, not guarantees. Always confirm current rates with a licensed loan officer and consult a tax or legal professional for advice specific to your situation. Past performance does not guarantee future results.